Before you sign a repair contract with a storm damage restoration contractor, ask the contractor for the name of the damage repair estimating program they will be using to estimate the cost of the repairs to your damaged property. If their answer is Xactimate® (or Symbility/Cotality), for the reasons described below, you need to find a storm damage restoration contractor who uses 3RStimax© that will price your damage repair work at real, true, and accurate (RTA) free market pricing that is relative to the insurance premiums you pay. To learn why this is extremely important, continue reading below

(3RStimax© is only available to restoration contractors certified to have completed the 3RSystems, LLC restoration contractor training program)

Just as the infamous and since pardoned Dr. Anthony Fauci was able to convince most of the planet that “masking up” was essential in protecting our physical health several years ago, through similar misleading tactics, over the past twenty or so years, the P&C insurance industry has convinced the majority of restoration contractors – many who are newer to the restoration industry, that using the so-called “industry standard” insurance adjuster mandated repair estimating program known as Xactimate (and, secondarily, Symbility/Cotality) was and is essential in helping them to achieve maximum repair accuracy and pricing. As illustrated in the “Weaponizing Xactimate” article through the PDF link directly below however, it is shown that, to the great detriment of insured commercial and residential property owners, their restoration contractors, the contractors building products distributors, and, just as important, the building product distribution company investors who were not previously but are now being made aware of the resulting tremendous building products sales deficits, neither of the above mentioned estimating products truly allow restoration contractors to achieve that goal.

“Weaponizing Xactimate: The Insurance Industry’s Dirty Little Secret”

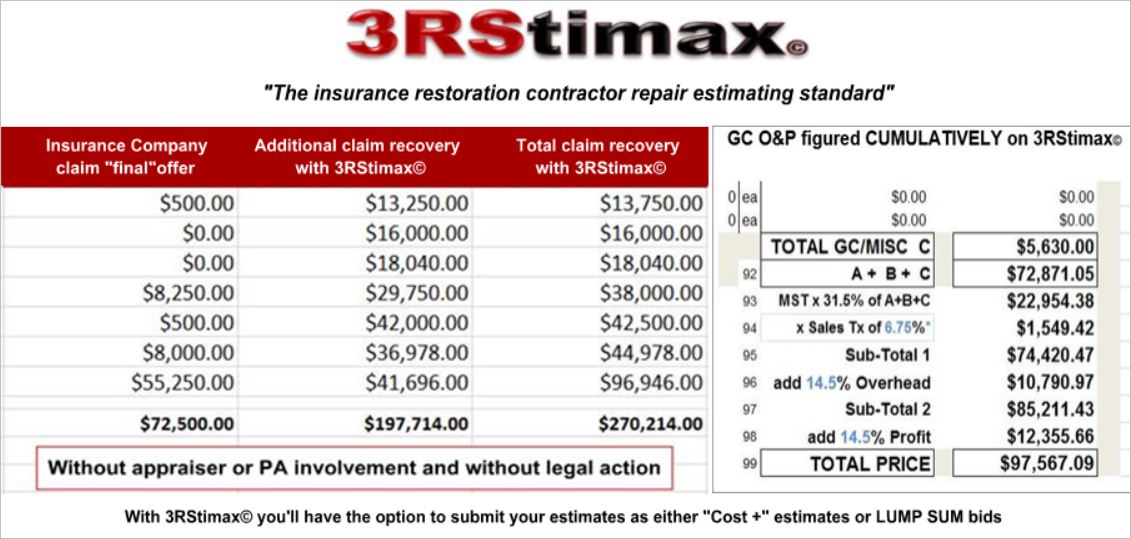

With the above in mind, the graph below clearly illustrates why restoration contractors who have bought into the Fauci-esque “the industry standard” repair estimating program is the best choice” mantra need to break free of those forced market, low ball, and insurance industry controlled damage repair estimating programs. Instead, they need to declare their independence by switching to using the non P&C insurance industry promoted, and contractor favored, 3RStimax© repair estimating program that allows restoration contractors to price their property owner customers insurance covered repairs at real, true, and accurate (RTA) free market pricing. In doing so, the restoration contractors’ customer’s are more likely to achieve fair, full, and complete settlements on their property damage claims which will then allow their restoration contractors to order all of the needed materials, complete all of the repair work, and hire the best installers. A comparison of the claim dollar recovery amounts shown in the graph below tells the whole story.

There is no rule or law that contractors must use “the industry standard” and, as shown below, there is no advantage in doing so.

(click on the above graph to enlarge)

(click on the above graph to enlarge)

Insurance “industry standard” repair pricing Vs 3RStimax© RTA free market repair pricing

After completing the advanced 3RSystems, LLC storm damage restoration contractor training program and switching from the now outmoded, so-called “industry standard” low ball and forced market priced repair estimating programs previously mentioned, as clearly illustrated in the 3RStimax© graph above, on just the seven insurance restoration projects shown, as a result of using the 3RStimax© contractor favored repair estimating program instead of one of those insurance industry adjuster mandated estimating programs, with the additional $197,714 recovered by the contractor, the final pricing paid by the insurance companies amounted to an astounding $270,214 – more than twice what the insurance companies had originally offered to pay the property owners.

Of that amount, along with the substantial increase in the contractors’ per job contract pricing, the roofing, siding, and related building products orders from the contractors’ building products distribution company were increased (on average) by $8,897 per job ($62,279 total). Also note to the right of the graph, the properly calculated General Contractor Overhead & Profit (GC O&P) payment totals.

Total additional claim recovery = $197,714

Total additional building product orders = $62,279

While the powerful and repeatedly proven 3RStimax© free market damage repair estimating program is an integral part of the full 3RSystems, LLC contractor training program, it is only a small part of it.

– STORM DAMAGE RESTORATION CONTRACTORS –

Fly higher, stronger, and faster with 3RStimax© from 3RSystems, LLC

INSURED PROPERTY OWNERS: Don’t allow your legitimate property damage insurance claims to be underpaid or denied because a contractor used the “industry standard” to estimate the damage repair costs. PRO RESTORATION CONTRACTORS: Learn more about what 3RSystems, LLC contractor training combined with 3RStimax© has done for other pro restoration contractors and their property owner customers from all across the USA. DISTRIBUTORS: See what 3RSystems, LLC/3RStimax© will do for you and your investors.

at:

![]()

(NOTE TO: ABC Supply Co. – SRS – HOME DEPOT – QXO – LOWES – and others: Your investors are starting to pay close attention!)

Copyright © 1996 – 2026 ICCOA / 3RSystems, LLC Minneapolis, Minnesota USA All rights reserved